Secret #37 – Fallacy of Geographic Composition – Foreclosures

Using The National Foreclosure Rate to Hide Local Truths

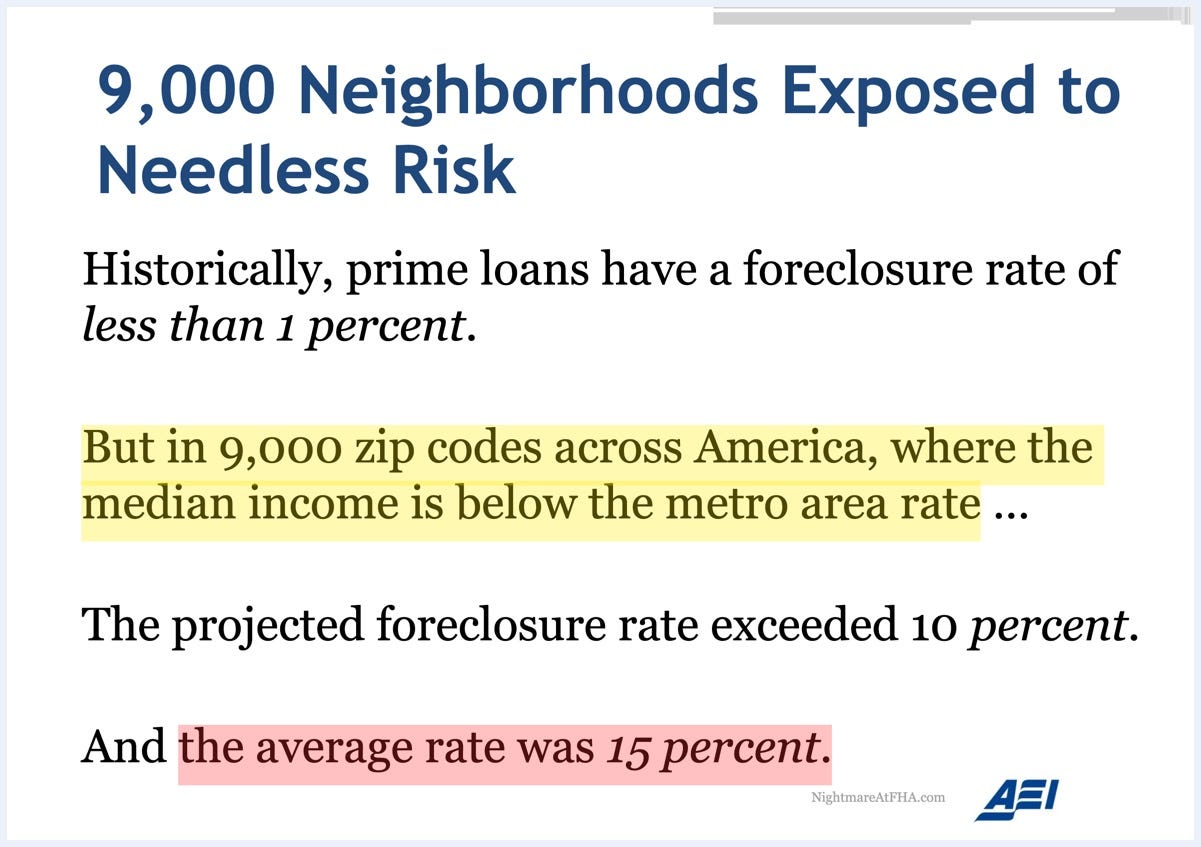

Source: Pinto. 2013. Annotated by Wake.

If those original policy changes that allowed house buyers to take on higher-foreclosure mortgages were targeted to lower-income home buyers, as is typical, then the price booms and price busts will be larger in areas with a higher concentration of those lower-income home buyers.

Then the eventual negative impacts of those changes will occur first and most in neighborhoods that have a higher than average concentration of recent, lower-income home buyers that used the higher-foreclosure mortgages.

“For the 25 percent of FHA borrowers living in the highest default rate zip codes, an estimated one in five lost their homes” (Pinto, 2016).

Higher-foreclosure mortgages don’t have much impact on your neighborhood if your neighborhood only has a few of them but if your neighborhood has a lot of them, it can be devastating when house prices stop increasing and foreclosures start increasing.

A high concentration of higher-foreclosure mortgages in a neighborhood means more neglected, vacant, abandoned, and eventually foreclosed houses, during real estate downturns compared to other neighborhoods that weren’t targeted and had fewer “affordable” mortgages.