Secret #39 – The Real Reason for “Affordable” Higher-Foreclosure Mortgages

“Affordable” mortgages are really Trojan Horses to increase home sales, not home ownership.

Mortgage lending standards are often lowered to boost the economy during recessions. Helping lower-income households may be the primary sales pitch but the timing suggests that’s not the primary motive. Here’s an example of home builder public relations in the 1950s with their pitch being that home building is the U.S. economy.

1940s and 1950s

Going into the 1948-1949 Recession, the law was changed which let FHA reduce the minimum down payment on new houses from 10% to 5%, and to increase the maximum mortgage length on new houses from 25 years to 30 years.

Right after the 1953-1954 Recession, the law was changed which let FHA reduce the minimum down payment on existing (not new) houses from 20% to 10%, and to increase the maximum mortgage length on existing houses from 20 years to 30 years.

Going into the 1957-1958 Recession, the law was changed which let FHA reduce the minimum down payment on new houses from 5% to 3%.

Foreclosures were EXTREMELY low in the early 1950s but became a problem in the early 1960s.

1960s

In 1968, in addition to promoting higher-foreclosure mortgages as helping lower-income home buyers, we start to see higher-foreclosure mortgages being promoted to help people of color, or as they said at the time, the “inner city.” Helping home buyers who are lower income and people of color is still the top justification for selling more “affordable” higher-foreclosure mortgages.

Section 235 of the Housing Act of 1968 loosened credit requirements for borrowers and allowed FHA mortgages that were “not intended to be actuarially sound” (von Hoffman, 2013).

1 in 8 FHA home buyers suffer foreclosure from 1975 to 2013.

1990s

Following the 1990-1991 recession, U.S. inflation-adjusted house prices were more or less flat for seven years and many housing policies were introduced, including “Affordable Housing Goals” for Fannie and Freddie that targeted lower-income and minority households.

The “Affordable Housing Goals” helped legitimize and support the non-prime, non-traditional, high-risk mortgage industry which was the primary cause of the 2000s real estate boom and bust, and the great length and depth of the Great Recession.

Do we exploit lower-income households in the long term to boost the economy in the short term?

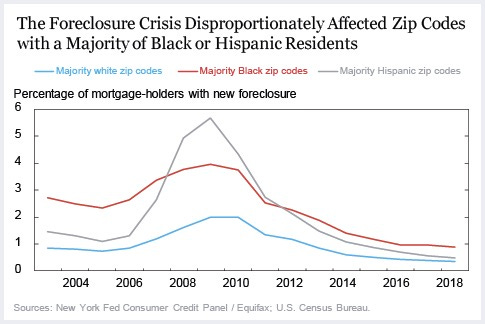

This is what I think of as “Blaxploition,” exploiting people of color to sell more mortgages and more new and existing houses in order to increase the profits of the real estate establishment in the short and medium run, but hurt lower-income home owners and home owners of color in the longer run, especially those who buy near the top of house price cycles.

Whether in China, Canada or the U.S., using housing policies to promote the economy instead of to promote sustainable, long-term, primary-home ownership, distorts the economy, as well as, home ownership.