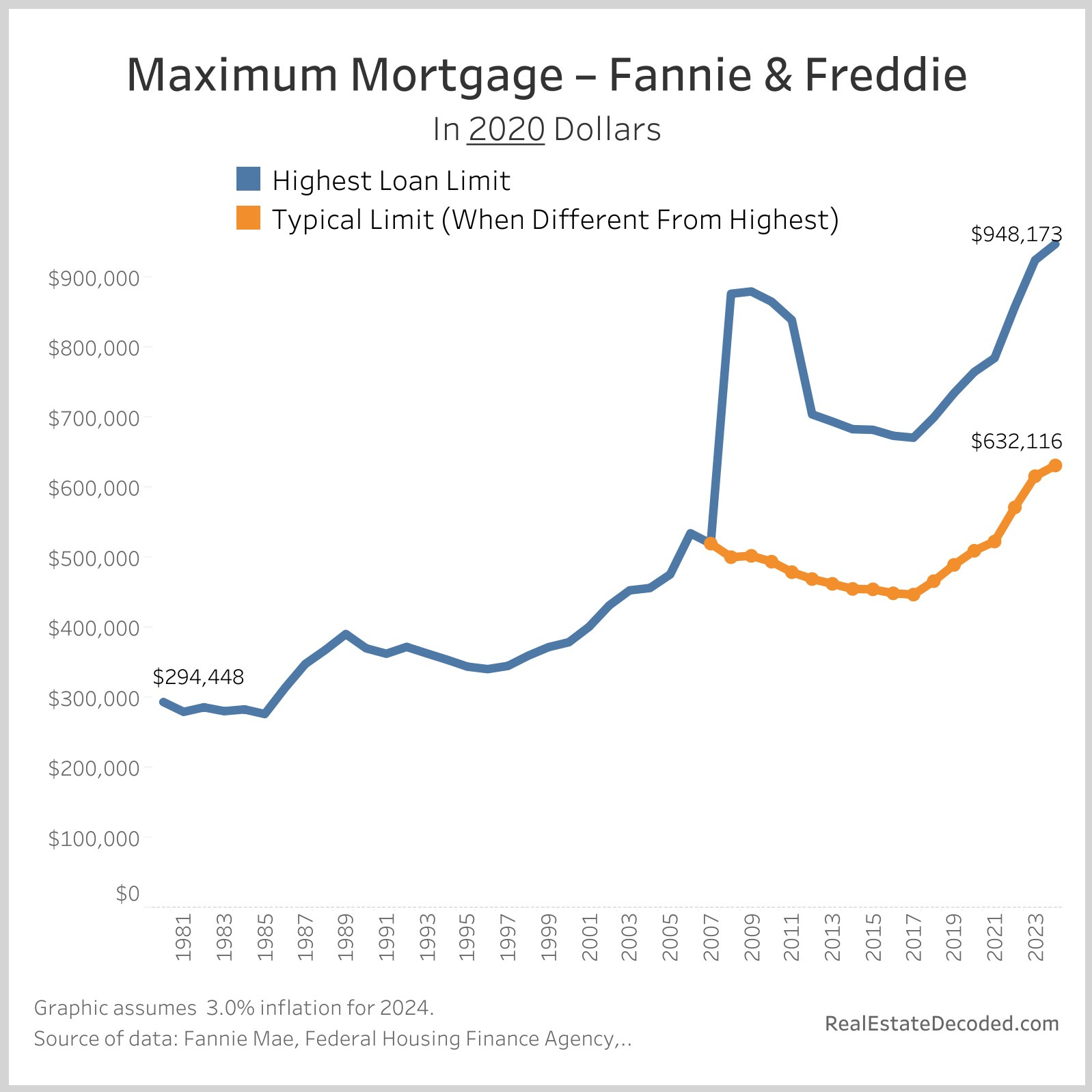

Secret #40 – Real, Inflation-Adjusted, Fannie & Freddie Loan Limits are 2 to 3 Times Higher Than in 1980

During the real estate bubble of the 2000s, Fannie Mae and Freddie Mac were involved, one way or another, in 44% of all U.S. mortgage debt outstanding.

And the maximum size of Fannie and Freddie mortgages increased 80% faster than inflation from 1980 to the peak in 2006. That increase in their loan limits helped enable the real estate boom of the 2000s.

If the loan limits on their implicitly federally guaranteed mortgages had only increased as much as inflation since 1980, developers would have built a lot more smaller, less expensive, new homes. In addition, the 2000s real estate boom and bust would have been smaller - maybe much smaller - if real loan limits hadn't increased so much.

Changing those loan limits from dollars to square feet would also help. If they really wanted to target first-home buyers, instead of increasing conforming loan limit dollar amounts every year, they could simply say houses have to be smaller than X square feet (1,750 square feet?) to be eligible. Then you rarely change that limit.

And see what happens to the number of smaller, more affordable new houses built.

And see smaller house prices increases.